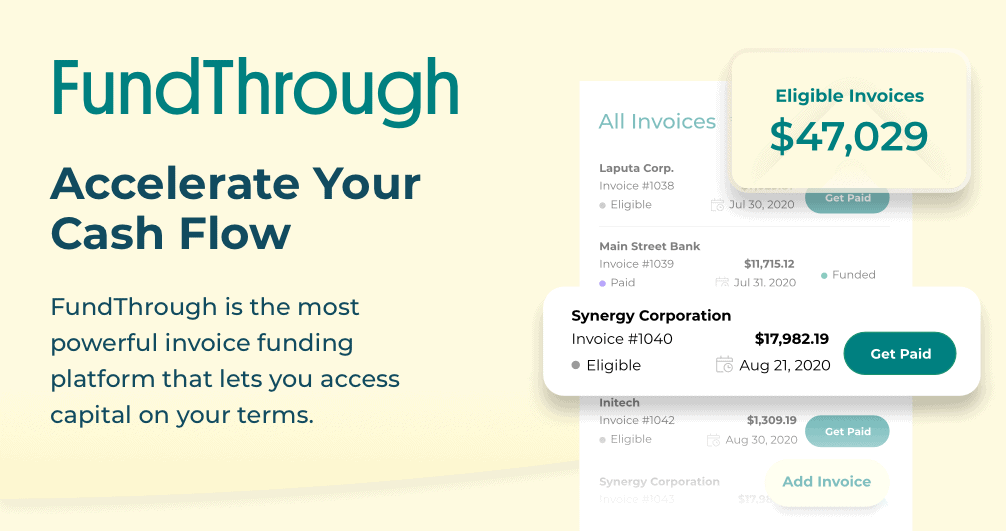

Accelerate cash flow to make payroll and grow your agency

Strong Canadian Support is Critical for Small Businesses to Survive—And Even Thrive—Amid Trump’s Tariff Chaos

READ

7 Best No Credit Check Business Funding Options: Success Tips for SMBs

READ

FundThrough Named Best Overall Invoice Factoring Company by Top Business and Finance Outlets

READ

Lima Charlie: Raising $8M in 30 Days to Unlock New Growth Channel

READ

Liquid Gold Trucking: Fueling 30% Growth in 18 Months With Early Invoice Payments

READ

FundThrough Ranked Number 415 Fastest-Growing Company in North America on the 2024 Deloitte Technology Fast 500™

READ