The 10 Best Banks for Small Businesses in 2025

Key Takeaways: Key Features to Look for in a Small Business Bank: Small business owners should prioritize customer service, security, competitive rates, and comprehensive features

Key Takeaways: Key Features to Look for in a Small Business Bank: Small business owners should prioritize customer service, security, competitive rates, and comprehensive features

Key Takeaways: Same-day business funding offers quick access to capital for emergencies, growth opportunities, and operational expenses, with options like invoice factoring, short-term loans, and

Canada’s small businesses are under siege. Ever since U.S. President Donald Trump announced a 25 percent tariff on Canadian imports, the fallout has been swift:

Key Takeaways Many alternative lenders offer business funding without conducting a credit check, focusing instead on business revenues and cash flow, providing a viable option

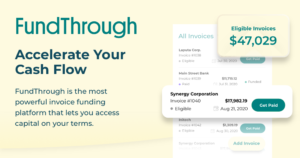

TORONTO – March 18, 2025 – FundThrough, a leading AI-powered invoice funding platform, has been recognized as the Best Overall Factoring Company by Forbes Advisor,

https://youtu.be/DwrNdfg3pHs When Ron Cedillo, VP of housing provider Lima Charlie, had to find new sources of business, he learned that the government contracting space