Thankfully, there are alternatives. Looking beyond the traditional sources of funding – stocks, bonds and cash – opens to the door to more flexible financing for your fledgling Canadian business.

Most alternative finance companies evaluate businesses seeking financing in non-traditional ways. They aren’t relying on your credit score or ability to fill out long forms to make a decision on whether to help finance your business. Because these aren’t traditional loan agreements, alternative finance companies can look beyond the simple formula of giving you money today that you will repay with interest in instalments over a certain period of time.

One option that seems popular on the surface is crowdfunding. Platforms like Kickstarter, IndieGoGo and RocketHub allow you to share your business idea with the world and solicit micro-investments from the ‘crowd.’ If you only read the occasional headline about a startup raising hundreds of thousands of dollars this way, it might seem like a viable financing option. However, while there are a few incredibly successful outliers, most crowdfunding campaigns fail. In fact, up to 89% fail to reach their funding target.

There’s an alternative that ensures you have cash flow when you need it, without sacrificing ownership and control of your new business. Invoice factoring is a small business finance solution that frees up cash you’ve already earned, so you don’t need to worry about having another monthly payment to cover over your initial years of business. No credit is required, as your creditworthiness is based on the strength of your sales. There’s no lengthy paperwork and approval process, and you don’t need to have collateral to obtain financing.

Explore FundThrough’s Ultimate Cash Flow Guide

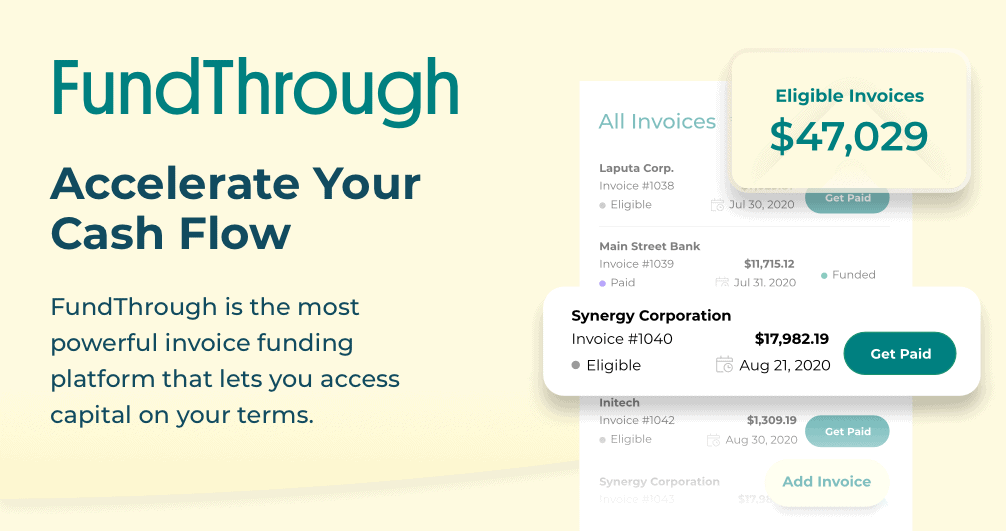

With FundThrough’s invoice factoring, you don’t need to convince anyone else of your new company’s viability. Your sales speak for themselves.

Here’s how it works. Once you’ve set up your account online, you simply connect FundThrough to your invoicing app and let us know where to deposit your funds. Within 24 hours, we’ll have reviewed your invoices and let you know what your initial limit is. We advance the funds you have already invoiced, so you don’t need to wait for payment. This allows you to extend reasonable payment terms to your customers, without sacrificing your ability to pay your expenses and employees, purchase capital equipment, and invest in the success of your new business.

You don’t need to rack up debt or put the success of your business in someone else’s hands. FundThrough’s invoice factoring gives you access to liquid capital you’ve already earned, when you need it most. As your business grows, we regularly reevaluate your account and increase your limit, so your financing grows with you.

Want to learn more? Take FundThrough for a test drive and see how simple capital financing can be, even if you’re brand new to Canada